Learn how salary packaging could be a way for you to pay less tax and have more money to play with.

Nobody enjoys watching their hard-earned pay get eaten up by tax. But if you’re a middle-to-high income earner, salary packaging could be a way to pay less tax and have more money in your pocket.

Here’s how it works.

The superannuation information in this article has been written by Australian Retirement Trust. Beam is part of Australian Retirement Trust group (ART). Together we’re working with your payroll provider to bring Australians closer to their super for a better retirement outcome.

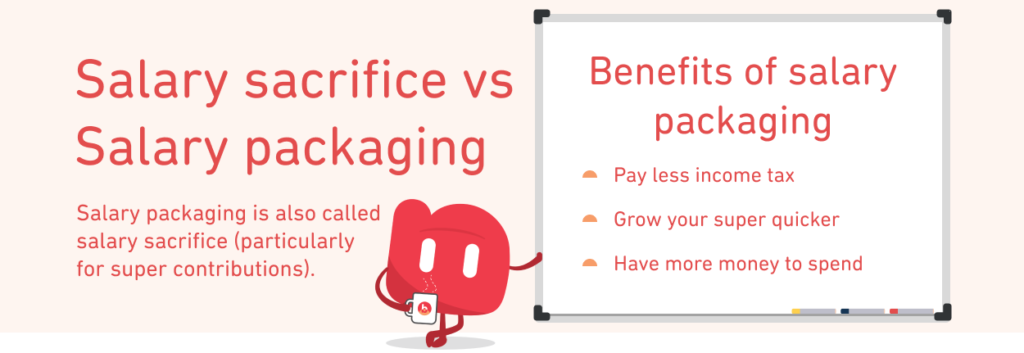

What is salary packaging?

Usually, you pay for expenses like bills, food and loans with your take-home pay after it’s taxed.

Salary packaging means you use some of your pay for certain expenses before it’s taxed.

This can include superannuation, cars, mortgage repayments and laptops, depending on your employer and the industry you work in.

By spending part of your salary before tax, you reduce your taxable income. And that may mean paying less tax – so you keep more of your salary. If you earn more than $45,000 per year, salary packaging super contributions could be a good way to power up your savings for retirement, depending on your circumstances.

Information provided by Australian Retirement Trust (ART) Learn more here.

How does salary packaging work?

Here’s a simple breakdown:

You and your employer agree on how much to salary package.

Your employer takes this money from your pre-tax salary to pay for or reimburse certain expenses.

The rest of your salary then gets taxed.

So, a salary package lets you pay for some things with tax-free money.

If you’re salary packaging superannuation, your employer pays this to your super fund as concessional contributions. Concessional contributions are taxed at 15% when they are paid to your super fund11 . There are limits on the amount of concessional contributions you can make each year.

Who can salary package?

Full-time, part-time and casual employees can use salary packaging as long as their employer offers it. Not all do, so you’ll need to check with your employer about what’s included in your workplace benefits program. Some of the benefits you can salary package are fringe benefits, and your employer might need to pay fringe benefits tax on these. They might ask you to make an employee contribution to reduce the tax they have to pay.

Keep in mind that the benefits of salary packaging depend on how much you earn. If you’re a low-income earner, there are less income tax benefits.

The ATO says that salary packaging may also affect things like:

the Medicare levy surcharge

some tax offsets

child support payments

some government benefits

study loan repayments that are compulsory.

Before you salary package, it’s a good idea to get financial advice from an accredited tax or financial adviser to work out if it’s right for you

What can I salary package?

Things you’d normally buy or pay for with your take-home pay can be part of a salary package. But it depends on the industry you work in and what your employer agrees to.

Common expenses in salary packages

Loan repayments

Rent

School fees

Health insurance

Mobile phone

What you can’t salary package

Any salary and wages, leave entitlements, bonuses or commissions that you accrue before the salary package agreement starts

Anything paid with direct debits from your pay

Salary packaging super contributions

Most employers will offer salary packaging for your super, even if they don’t offer it for other things. But if you’re a low-income earner, you might not get the tax benefits of salary packaging. Instead, you can grow your super in other ways, like making after-tax contributions.

Is salary sacrifice right for you?

Salary sacrificing might help you save on tax and grow your super.

The ATO may apply an extra 15% tax to some or all of your contributions if your income plus concessional contributions is over $250,000 per year. ↩︎

The information on this website contains general information only. It doesn’t consider your personal objectives, financial situation, or needs. Before making any decisions about ART, you should read the relevant Product Disclosure Statement (PDS) and Target Market Determinations (TMD) to consider whether the product is right for you.

This is general information. It’s not based on the specific objectives, financial situation or needs of your business. So think about those things and read the Product Disclosure Statement before you make any decision about our products. Contact your payroll provider for a copy of Product Disclosure Statement (PDS).

Beam is issued by Precision Administration Services Pty Ltd (Precision) (ABN 47 098 977 667, AFSL 246 604). Precision is wholly owned by Australian Retirement Trust Pty Ltd (ABN 88 010 720 840, AFSL 228 975), trustee of Australian Retirement Trust (ABN 60 905 115 063).

We’re careful with your personal information. Our privacy policy explains how we handle it. You can find it at beamconnect.com.au/privacy

Whether you’ve registered and are preparing to make your first payment, or you want to understand more about how Beam works, here’s a look at how to make super payments using Beam. Beam connects to your payroll software, then does the hard work for you by tracking and calculating employee super amounts as you pay […]

As retirement costs rise, Beam makes super payments super easy. Over the past 20 years, the cost of a comfortable retirement has gone up by a staggering 75%.1 Many of your employees will be wondering what that means for their life after work – but there are things you can do to help them boost […]

Want to streamline your super payments? Start by looking at your data

The words ‘data management’ might not spark much excitement, but keeping your information well organised can make it much easier for you to meet your obligations. As an employer, paying super probably isn’t your top priority. After all, you’ve got a business to run. But streamlining your super payments will help you to get more […]